Photo by Xavier Lejeune on iStock

Key Points

- On April 24, the EU Parliament formally approved the CSDDD, a major milestone in the global advancement and harmonization of responsible business conduct standards, promising to help companies respect human rights, and achieve climate and other environmental goals.

- Risk-based due diligence offers a pragmatic approach for companies to prioritize actions and resources, focusing on their most severe and likely impacts; and strengthens their ability to identify material issues for compliance with reporting obligations.

- Three elements of the law will require a step change in business practices: full supply chain coverage, meaningful stakeholder engagement, and environmental due diligence.

After several years of negotiation, the EU Parliament has formally approved the Corporate Sustainability Due Diligence Directive (CSDDD), which will be formally adopted shortly. Companies in scope have until 2027 at the earliest to comply with its provisions.

CSDDD comes against a backdrop of growing societal inequality intensifying conflict, and worsening environmental degradation with devastating consequences for people whose lives depend on natural resources. Together with the Corporate Sustainability Reporting Directive (CSRD), this is the most comprehensive and ambitious attempt to consolidate and harmonize businesses’ responsibility for their impacts on people and the planet.

Although the Directive will apply only to very large companies (including non-EU companies generating over 450m in turnover in the EU), its impact will extend across global supply chains. Companies in scope—an estimated 5,500 in the EU alone—will have to inspect their operations and their direct and indirect business partners to identify, assess, and address human rights and environmental harms connected to their activities. By adopting the concept of risk-based “due diligence”, in line with the OECD Guidelines for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights, CSDDD promises to help companies respect internationally recognized human rights and achieve environmental goals.

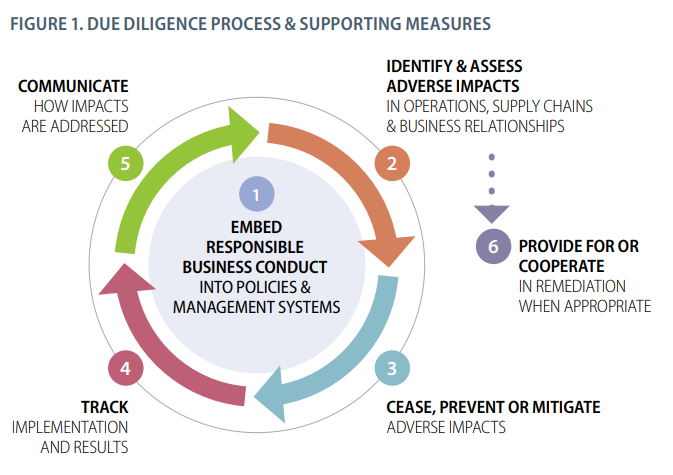

The six-step due diligence approach set out in the OECD Guidelines is reflected across the CSDDD:

- Integrating due diligence into policies and risk management systems (Article 7).

- Identifying and assessing actual or potential adverse impacts, prioritizing potential and actual adverse impacts based on severity and likelihood (Articles 8 and 9).

- Preventing and mitigating potential adverse impacts, and bringing actual adverse impacts to an end (and minimizing their extent) (Articles 10 and 11).

- Monitoring the effectiveness of due diligence actions (Article 15).

- Publicly communicating on due diligence (Article 16).

- Providing remediation for actual adverse impacts (Article 12).

Source: OECD Due Diligence Guidance for Responsible Business Conduct

In practice, companies of all sectors are connected to a wide range of adverse impacts through their own operations and business relationships. Recognizing that companies may not be able to address all these impacts simultaneously, CSDDD allows them to prioritize action based on the severity and likelihood of impacts on affected people and environments.

This pragmatism extends to how companies will be held accountable. Where a company causes or contributes to (‘jointly causes’) harm, they must remediate the harm and may be liable for damages. A company that is linked but didn’t directly cause or contribute to the harm can build and use its influence to prevent or mitigate the harm but is not required to remediate and is not subject to damages. However, since addressing actual impacts involves remediation, businesses should use their influence to enable it.

The CSDDD will require a step-change in business practices

From our experience working with companies to implement due diligence in line with international standards, a few provisions of the CSDDD stand out as meriting particular attention from companies.

1) Full supply chain is in scope

Due diligence is not limited to direct tier 1 suppliers. Companies must take a risk-based approach to managing impacts across their full supply chain. This means mapping and testing the effectiveness of supplier risk management systems to identify “general areas where adverse impacts are most likely and most severe” (Article 8) and investing resources to deepen assessments of those areas. If the most severe or likely impacts are connected to raw materials extraction, then that is where further attention is required.

Recognizing the challenges in addressing impacts far down in supply chains, CSDDD recognizes multi-stakeholder and industry initiatives as tools for increasing leverage to identify and address impacts. However, companies must monitor the effectiveness of initiatives to ensure they fulfil their obligations.

2) Meaningful engagement with affected stakeholders is necessary

Meaningful stakeholder consultation is required throughout the due diligence life cycle. Stakeholders include workers and other people affected by business—and their legitimate representatives (including trade unions, civil society organizations and human rights defenders)—as well as national human rights and environmental institutions and civil society organizations working on environmental protection.

To ensure genuine interaction and dialogue, companies must provide consulted stakeholders with comprehensive information, plan ongoing consultations, address barriers to engagement, and ensure stakeholders are free from retaliation and retribution.

This approach will require a significant shift in how companies structure and conduct engagement. It will involve building or deepening relationships and identifying opportunities for continuous engagement at each step of due diligence—while addressing the increased burden this may place on civil society, trade unions, and others representing affected people and the environment. Companies will need to be more transparent with affected stakeholders, reduce power imbalances, and engage in good faith with critical voices who raise concerns.

3) Environmental due diligence and the intersection with human rights

Historically, in the environmental field, the term due diligence has had a distinct meaning from that of sustainability due diligence: referring to technical, scientific site-specific evaluations of environmental conditions and impacts. More recently, leading environmental frameworks used by companies, such as the Science Based Target for Nature framework, have been based on similar processes—of identification, prioritization, action, and monitoring—to the due diligence approach in CSDDD. Moving forward, articulating how a company assesses and prioritizes its environmental impacts using the lens of severity and likelihood—and integrating meaningful stakeholder engagement—will require concerted efforts and innovation.

The CSDDD also requires companies to address the impacts of environmental degradation on human rights, including the rights to health, food, and clean water and sanitation. This requires bridging environmental and human rights teams—who operate largely in siloes today—to identify and more effectively manage these interconnected impacts.

In this new era of sustainability regulation, the CSDDD is a gamechanger. But delivering on its ambition will require clear commitment, robust governance, and sufficient resources from companies, including truly cross-functional efforts. BSR looks forward to supporting companies in stepping up to this challenge, through continued analysis and promotion of best practices.

BSR’s latest sustainability insights and events straight to your inbox.

Topics

Authors

Diana Wilkinson

Former Global Lead, Supply Chain, BSR

New York

Beth Richmond

Former Director, Transformation, BSR

New York

Resilient business strategies for a complex world.