Introduction

Companies offering leather products can face direct and indirect risks of deforestation and land conversion. Businesses that supply them with leather goods might be sourcing leather from farms where forests have been cleared or natural lands have been converted to make way for cattle farming—a direct deforestation risk. Or, if the leather was sourced without direct deforestation or conversion from cattle rearing, the company could still be indirectly exposed to deforestation or conversion on land that was used to grow cattle feed.

The member companies of the Responsible Luxury Initiative (ReLI) in aggregate source significant volumes of leather from European countries compared to volumes from countries in other regions (e.g., South America). For cattle raised in European countries, direct deforestation or land conversion is not a primary concern. However, cattle raised on European ground could be fed with soy cultivated in South America, where forests have been cleared or lands converted to make space for agriculture. This creates an indirect link from European cattle leather sourcing to deforestation and land conversion. Because indirect links have not been well studied or understood, ReLI members decided to explore this topic.

Furthermore, the impending EU Deforestation-Free Supply Chain Regulation makes this a legal requirement. According to the regulation, deforestation-free expectations will apply to products that contain, have been fed with, or have been made using the commodities in scope. Operators placing in-scope products (referring to products in Annex 1 of the European Union Deforestation-Free Supply Chain Regulation) on the EU market must ensure that the feed is deforestation-free as part of their due diligence. When it comes to the leather supply chain, there are several products in scope, including live cattle and leather, at various stages of processing. In our interpretation, the operators responsible for due diligence related to soy feed will include cattle farmers, slaughterhouses, tanneries, leather producers of unfinished products, and brands who own any of these value chain stages.

Leather is likely to be one of the luxury industry’s raw materials with the highest deforestation risk; cattle production was identified as the largest driver of global deforestation by World Wildlife Fund. Although leather is a by-product of the beef industry and is not solely driving deforestation from cattle, leather buyers remain key supply chain players, are exposed to deforestation risk, and have a responsibility to address it.

ReLI investigated the deforestation risk linked to its members’ leather supply chains via soy in cattle feed. This research is focused specifically on soy that is embedded in leather sourced from Europe. Its objectives were to:

- Build a stronger understanding of the various implications of members’ sourcing activities

- Consider the most effective role members can play in working toward elimination of soy deforestation and land conversion given their downstream position.

The investigation entailed three key research steps:

- In partnership with Trase, we sought to understand the deforestation risk of soy embedded in the leather supply chains of ReLI members.

- We leveraged desk-based research to complement the Trase results to better characterize the risk for priority leather-producing countries (France, the Netherlands, Italy) and discuss opportunities to tackle soy deforestation and land conversion.

- We discussed our findings with deforestation experts to develop a view on the actions the industry can take to address soy deforestation and land conversion.

In this case study, we share the high-level results of that research and proposed next steps for action.

Establishing Transparency

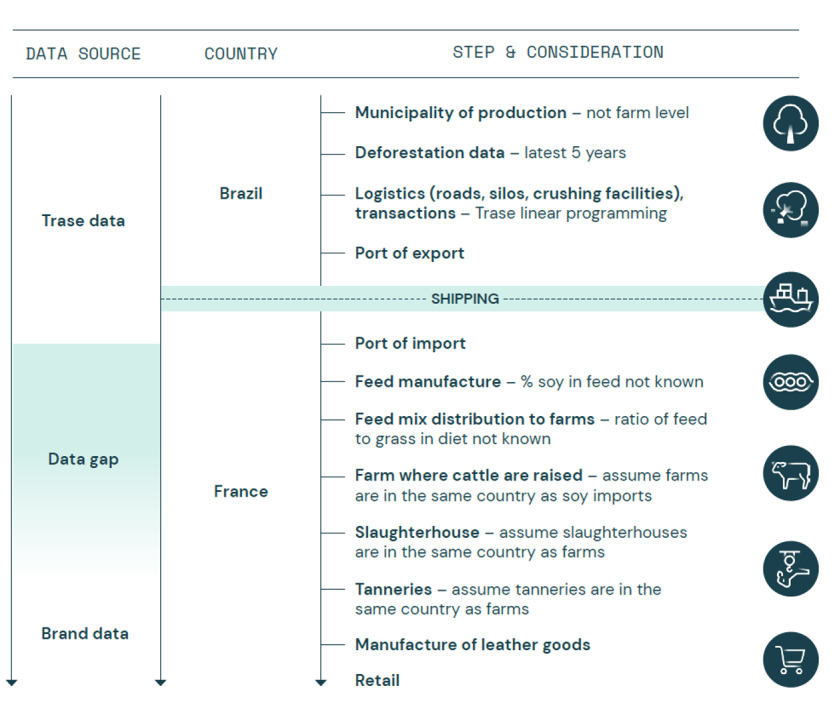

In 2020, ReLI worked with Trase, a supply chain transparency initiative led by the Stockholm Environment Institute and Global Canopy, to gain better transparency into the levels of soy deforestation risk linked to their leather supply chains. In November 2022, Trase replaced the term "deforestation risk" with "deforestation exposure" as a measure of the exposure of supply chain actors to deforestation from commodity production based on their sourcing patterns.

Five ReLI member companies provided supply chain data to Trase, including the locations where they source leather, associated volumes of material, and locations of related actors in their supply chains. Location can refer to a farm, slaughterhouse, or a tannery, depending on the level of traceability of a given member company. The level of traceability was mixed, similar to the broader industry—some companies had visibility to farm level, others to tanneries or slaughterhouses. As expected, traceability to feed level was lacking. ReLI learned that France, the Netherlands, and Italy were the top leather-sourcing countries in aggregate for its members that provided supply chain data to Trase.

Trase's database has information on commodity flows, including data on production of soy in Brazil, Paraguay, and Argentina (three of the major soy producing countries with risk of deforestation), deforestation rates in these locations, and trade/export data to link soy deforestation to leather-producing (soy-importing) countries of interest. Members' supply chain data was combined with the Trase data, resulting in an estimate of soy deforestation risk exposure (at an aggregate and for each brand) associated with soy sourced from Brazil, Paraguay, and Argentina. This data was used to identify deforestation risk “hotspots” that would be priorities for supply chain or landscape-level attention. Figure 1 shows the data considered in the calculation and presents the analysis’ data gaps. These data gaps required making assumptions in the calculation of deforestation risks. For example, if companies were not able to provide data on the farm where cattle were raised, where reasonable, Trase assumed that downstream processing suppliers (e.g., abattoirs) were themselves sourcing locally.

Source: Trase

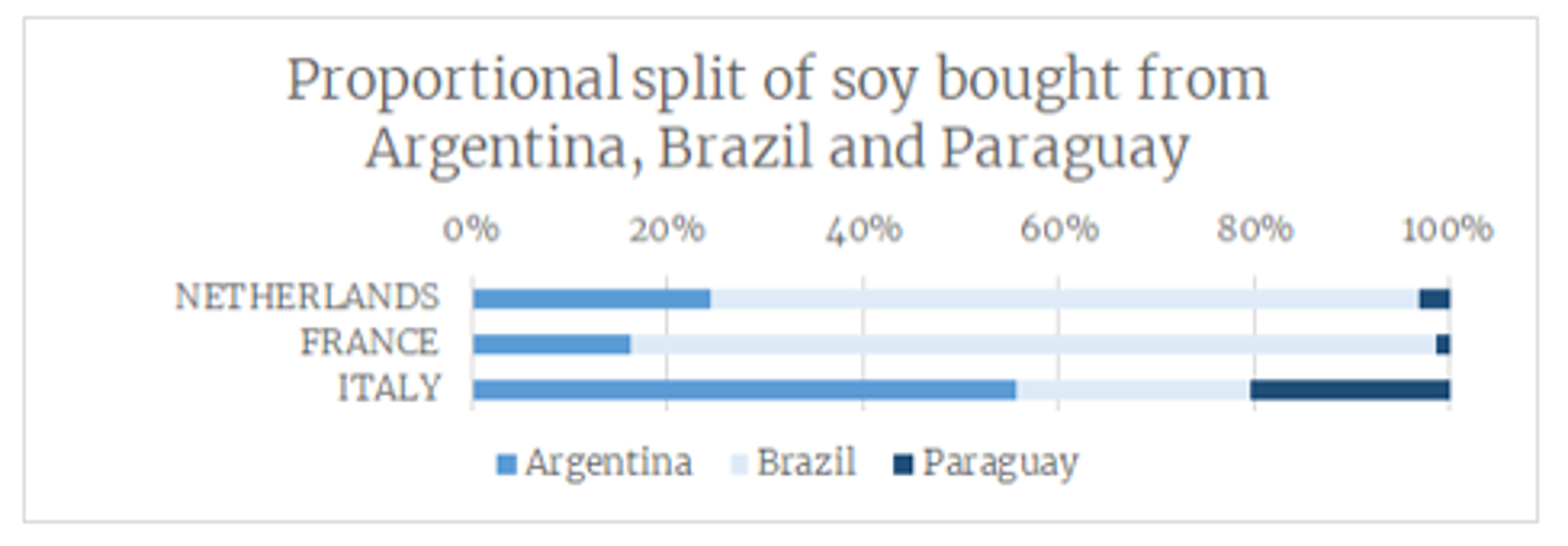

The Trase analysis identified clear differences in relative risk exposure across producer countries (those producing soy) and supplier countries (those potentially using/importing soy and supplying leather), but also areas of overlap around “hotspots” of risk. ReLI learned that the risk exposure is quite variable across source regions and countries importing soy. For example, the average deforestation risk in Paraguay (11.7m² per tonne) was higher than in Brazil (6.6m² per tonne) or Argentina (0.58m² per tonne), but European countries tend to source proportionally less soy from Paraguay (see Figure 2 for the sourcing percentages). Brazilian soy imported into Europe had a higher deforestation risk than the average deforestation level attached to soy produced in Brazil. This could be because Europe’s historic trade routes were linked to areas in the country that had higher deforestation rates. For example, for France, the deforestation risk attached to soy imports from Brazil was 9.08 m² per tonne, compared to 6.6m² per tonne on average. The details are summarized in the Figure 3.

Source: Trase

Figure 3: Deforestation Risk per Country

Source: Trase

|

Soy Production Country |

Average Deforestation Risk (m² per tonne) |

Deforestation Risk for Soy Imports |

||

|

France |

The Netherlands |

Italy |

||

|

Brazil |

6.6 |

9.08 |

7.12 |

9.91 |

|

Argentina |

0.58 |

0.66 |

0.60 |

0.69 |

|

Paraguay |

11.6 |

9.8 |

11.6 |

14.8 |

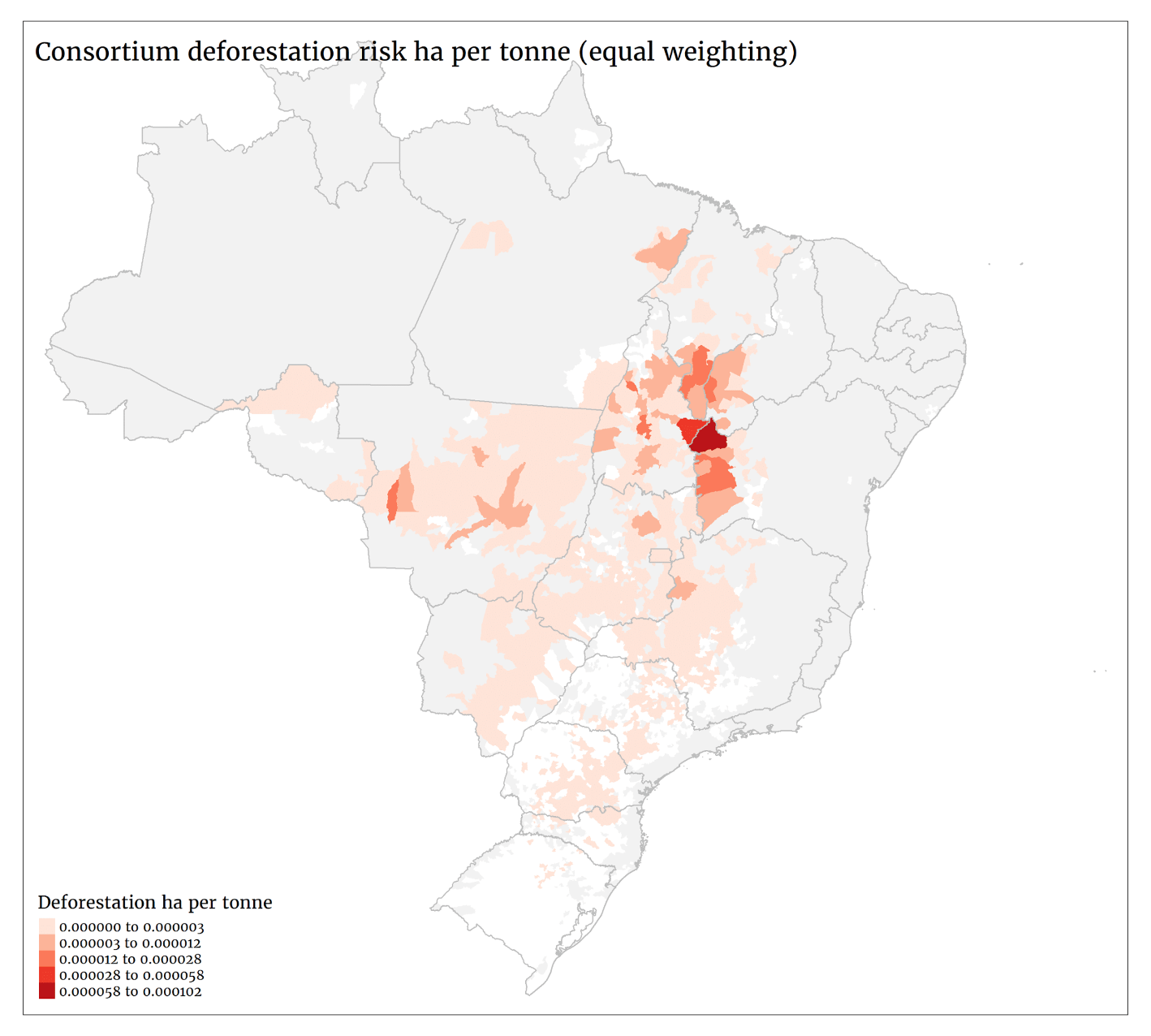

Figure 4 depicts the type of information we received from the Trase analysis of company data. The map indicates the deforestation risk in hectare per tonne for the ReLI consortium. In other words, it presents the distribution of deforestation linked to one tonne of soy bought in proportion to the ReLI companies’ sourcing patterns (i.e., weighted by volume of leather sourcing). Similar maps were provided for soy from Brazil, Argentina, and Paraguay at an individual company level and collective group level. Without traceability to feed level, it is not possible to be certain on the deforestation risk associated with members’ supply chains. However, by drawing on a science-based metric to assess exposure to deforestation in supply chains, Trase can provide a plausible map based on information on production, trading, and other data from countries in members’ supply chains. Such findings are useful for targeting engagement with suppliers on deforestation.

More information on the Trase analysis can be found here.

Figure 4: ReLI Consortium Deforestation Risk per Tonne Bought from Brazil

Source: Trase

Characterizing the Risk

The ReLI team complemented the Trase analysis by studying cattle farming systems, feed profiles, and use of soy for the top leather-producing countries for the ReLI members that provided data (France, the Netherlands, and Italy).

First, we wanted to supplement the Trase data with additional quantification. From Trase, we received an estimation of the deforestation risk (m² of land per tonne of soy) for soy imported from Brazil, Paraguay and Argentina into France, the Netherlands, and Italy. However, not all imported soy is used for cattle feed—it may also be used for other livestock feed or for humans. One element of this research was to explore how imported soy is used in ReLI’s three priority leather-producing countries so that we could understand how important the risk of leather-linked deforestation via soy might be.

A key challenge was that publicly available data on the amount of imported soy that leather-producing countries used for cattle feed was difficult to find and/or rely on. As a result, we could not make an accurate estimation of the soy deforestation risk linked to cattle in these countries, though we feel confident in the general takeaway: While general global risk of deforestation due to soy production may be high, leather-linked soy deforestation risk across countries and companies is extremely fragmented. All companies sourcing forest-risk commodities in their supply chains have a responsibility to protect forest landscapes, but fragmentation of impact will limit individual influence. Collective action is needed.

Second, we developed a better qualitative understanding of the farming systems in the prioritized leather-producing countries to help us contextualize the soy use in cattle feed. For example, understanding the extent of intensive farming systems (high inputs compared to land area) versus extensive (more land under cultivation with lower inputs), or indoor versus outdoor cattle rearing, can help inform the best approach to engaging farmers on changing feed inputs.

Since the luxury industry commonly uses calf leather, we also investigated any unique considerations for calf rearing. For example, we confirmed that soy is used in calf feed and that the Netherlands is an important focal country for industry deforestation efforts considering its high levels of veal production and likely higher soy-related deforestation risk.

Finally, we identified several existing programs in France, the Netherlands, and Italy working to address soy deforestation, allowing us to think through opportunities for our members to work on farm-level initiatives in their supply chains.

Some sample high-level results of this research can be found in Figure 5.

|

France |

The Netherlands |

Italy |

||

|

France has the largest cattle farming system in Europe, meaning the most beef and dairy cows in the system, and is the second largest production country for veal (28 percent). Both beef and dairy cows are mainly fed grass over their lifetimes, though soy makes up anywhere from 0.6-2.5 percent of the cattle feeding system. France has a highly extensive system. The average farm in France has 56 cows, with more than half of the farms having 5-49 cows. |

The Netherlands is the top production country for veal in Europe (36 percent). The Netherlands has had intensive cattle farming systems—more than 3 in 10 Dutch cows were kept permanently indoors in 2012—but legislation is pushing the evolution toward extensive techniques. The dairy farming sector is the largest land user in the country, taking up 0.9 million hectares of land. The Dutch dairy sector collectively committed to 100 percent responsible soy and achieved this by requiring the purchase of Round Table on Responsible Soy (RTRS) credits in delivery terms. Only animal feed suppliers that buy credits for responsible soy are permitted to supply feed to Dutch dairy farmers. |

Italy is the fourth largest beef producer in Europe and the third largest production country for veal in Europe (13 percent). Farm sizes vary between regions, though there is a notable intensive system. Italy has been known for its role in the fattening stage. The Italian strategy of “safety from farm to table” from the Ministry of Health aims to ensure transparency of the supply chain to the farm level and between various actors, whether produced in the EU or imported. |

||

|

|

|

|

||

Impact

The completed research helped ReLI members better understand, define, and raise the visibility of the risk of embedded deforestation and land conversion related to their leather supply chains—a topic that previously was not fully understood. Companies indicated that this research is helpful for informing steps to expand the scope of individual deforestation and conversion commitments to include embedded materials, supporting companies in addressing all areas of significant risk. Companies also indicated that it has been helpful in establishing comprehensive corporate biodiversity strategies (e.g., aligned with SBTN).

The ReLI team presented this study to NGOs and deforestation experts to get their perspectives on the most effective role ReLI members can play in addressing soy deforestation. Stakeholders highlighted the brand influence of luxury companies and of groups such as ReLI, especially when working collectively, and the importance of them playing a role. Still, they did recognize that luxury companies are far downstream, and thus ReLI brands should clarify why they want to engage in soy-related deforestation and that collaboration with major sector players such as beef, dairy, and food retail will be key to enabling action.

Next Steps

First, ReLI would like to acknowledge the Call to Action released from Textile Exchange and Leather Working Group for companies to commit to deforestation- and conversion-free leather by 2030 or earlier. ReLI is supportive of this Call to Action; several ReLI members will align their leather deforestation commitments to those expectations. Based on the findings of this case study, ReLI also encourages companies to look beyond direct deforestation risk and expand the scope to embedded materials in leather supply chains, using the work described in this case study to inform their approach.

Recognizing the remaining data and traceability challenges, in 2023, ReLI will engage with key supply chain players (which may include France-, Netherlands-, and/or Italy-based slaughterhouses, farmer groups, feed initiatives, or other trade associations) to identify and evaluate ways that downstream companies like luxury brands can support tanneries, slaughterhouses, farmers, or other relevant players in the due diligence needed to achieve deforestation-free feed. These engagements will also prioritize opportunities for coordination with downstream players in the meat industry. ReLI will share additional relevant insights for the industry as this work continues.

This case study reviews a piece of work completed by the Responsible Luxury Initiative (ReLI) in 2022. ReLI is a collaboration of luxury sector companies. Its mission is to provide a platform to discuss, explore, and develop collaborative solutions for persistent and emerging sustainability issues in their value chains.

This case study was written by Cliodhnagh Conlon, Ricki Berkenfeld, and Sarah Cornelles, with guidance and insights provided by select ReLI members. The authors wish to thank Trase for collaborating on the research presented in this case study.

Please direct comments or questions to Cliodhnagh Conlon.

Resilient business strategies for a complex world.