Searching for:

Search results: 151 of 1242

Blog | Tuesday April 8, 2025

Navigating Uncertainty: The Impact of U.S. Tariffs on Sustainable Business

The overall impacts of the U.S.‘s announced tariffs will almost certainly seriously impede sustainable business. Explore the potential consequences of the tariffs and how companies can respond effectively.

Blog | Tuesday April 8, 2025

Navigating Uncertainty: The Impact of U.S. Tariffs on Sustainable Business

Preview

Updated on June 25, 2025 to include the impacts of the U.S. tariffs on energy, extractive, transportation, and industrial companies.

Energy, extractive, transportation, and industrial (EETI) companies are critical to advancing sustainability around the world. Due to their deep integration with global supply chains, EETI companies are particularly attuned to volatility in trade conditions, such as the U.S.'s recent tariffs. This uncertainty and volatility will undoubtedly impact workers and the advancements that companies have made on integrating labor rights into their business models.

The United States’ announcement that it would be imposing tariffs on all nations will affect all aspects of global trade, most certainly including sustainable business.

There is widespread uncertainty about whether these tariffs are permanent, or rather an effort to force negotiations, or some unpredictable combination of the two. Given this, the impacts on sustainability are in some cases unclear, though some impacts can be predicted with a high degree of certainty. But while the predictability of individual impacts is unclear, the overall impacts are almost certainly a serious impediment to sustainable business.

Should the tariffs remain largely in place, impacts will likely include:

- Job losses in exporting countries where they are badly needed: Economic growth in countries like Vietnam and Cambodia are in large part a result of their increasingly important roles in global supply chains. Should their export industries be hit hard, it will create social and economic dislocations, which will disproportionately hurt women, who have been able to enter the formal work sector through export industries.

- Economic disruptions to materials needed to accelerate clean energy: Global trade, whether in minerals or components for the clean energy economy, will be sharply reduced by these tariffs. Many business leaders are now predicting a recession in the U.S., and a drag on economic activity globally. This would almost certainly raise the price of, and slow down, the energy transition.

- Reduced attention on labor and economic conditions in global supply chains: With global supply chains in turmoil, getting products to market through whatever means necessary could reduce the attention paid to ensuring that labor rights and other human rights are respected.

Even if the tariffs are largely or entirely reversed in short order, there will be lasting damage to the sustainable business agenda because we will see:

- Heightened geopolitical conflict: The tariff policy is resulting in yet more tension in the global system. In addition to the immediate threats and realities of countervailing tariffs from other countries, deepening divisions in the world mean that the global cooperation needed to advance core principles of sustainable business (Trans-Pacific Partnership, anyone?) is on life support. This will be on display at COP30, as well as in other fora.

- Diminished access to critical inputs: Energy, extractive, transportation, and industrial companies play a vital role in global sustainability efforts, but they are highly sensitive to trade volatility due to their deep ties to global supply chains. Disruptions like tariff uncertainty can threaten their access to critical inputs, such as rare earth minerals and clean energy components, which are essential for technologies like EVs, batteries, and solar panels.

- Managing volatility and uncertainty crowds out sustainability in the boardroom and C-suite: Simply put, the business agenda is full to bursting right now. Economic uncertainty, flagging consumer sentiment, and the rise of generative AI is straining both the bandwidth, and the budgets, which companies are able to deploy on sustainability. This is clearly short-sighted, and there is zero doubt that the urgency and importance of sustainability will reassert itself. But time, like money, is a finite resource, and for the time being, there are many demands on decision-makers.

- Declining support for rule of law and human rights: The U.S. has been an abiding—if imperfect—voice for rule of law and human rights in global trade. Its voice on these matters is now silent, if not discredited for a generation or more. Taking the world’s largest economy and voice out of this debate is deeply damaging for anyone interested in advancing an economy based on rules. Companies headquartered in the U.S. are also likely to face a loss of credibility on such matters.

These are all the ways that sustainability is challenged by tariffs. But, as Albert Einstein once said, in the middle of difficulty lies opportunity. This blow to the economic system reinforces the importance of resilience, and scenarios as a tool for navigating uncertainty.

The volatile economic impacts of the tariffs should remind all of us that the needs of people must always be central to the sustainable business agenda. Yes, the Trump administration is the proximate cause of this disruptive chapter in the global economy. But it is also important to pause and consider why so many in the public have lost faith in global free trade, creating the environment in which tariffs appeal to many. Large segments of the public long ago abandoned the idea that globalization will make their lives better. They see trade as decimating jobs and communities and heightening their vulnerability—turbocharged by technology—to forces beyond their control.

The business community has an important role to play in demonstrating—with actions, not only with words—that an integrated global economy is the best system for meeting the needs of the average person. Business should not only stand up for global trade, but it should also make sure it works better for more people. This means business support for a modernized and reliable safety net, advocacy for democracy and rule of law, and a plausible vision of employment in an age of AI. Short of that, large segments of the public will support trade barriers that run afoul of the system most companies believe in.

The impacts of tariffs on sustainable business are not easy to predict. The tariffs have introduced even more volatility into an economy facing substantial change. Business may not be able to persuade the American administration to reverse course. But it can take immediate steps to mitigate harms arising and refocus on creating business models, and an economic system, that has opened the door for political support for these tariffs—however misguided—in the first place.

Blog | Thursday April 3, 2025

Fintech: Managing Human Rights Risks to Maximize Social Benefits

Fintech is a booming industry that allows a secure, convenient, and accessible use of financial services, but its opportunities come with social and human rights risks that companies can address through a tailored approach aligned with the UNGPs.

Blog | Thursday April 3, 2025

Fintech: Managing Human Rights Risks to Maximize Social Benefits

Preview

Financial technology (“Fintech”) refers to technology that financial services companies use to make their products and services more secure and widely available. It has transformed a historically slow, high-barrier industry into a faster and more accessible global financial system through a range of innovations, from mobile applications and payment platforms to digital currency and specialized algorithms to analyze data and insurance risk. The industry exhibited an average growth rate of over 50 percent from 2020 to 2022, with projected strong global growth into the future.

In digitizing the financial services industry, one of fintech’s primary benefits has been increasing financial inclusion. The UN Department of Economic and Social Affairs advocated for digital financial solutions as a method for achieving financial inclusion under the 2030 Sustainable Development Goals (SDGs), given its potential to help eradicate poverty and foster gender equality and economic independence for women.

However, fintech opportunities also pose significant social and human rights risks, which can have negative impacts on people, as well as reputational, legal, and regulatory consequences for companies. In light of fintech’s rise and potential to affect billions of lives, it is critical that fintech companies, or fintechs, evaluate and address negative social and human rights implications associated with its deployment to maximize the societal and economic benefits offered by these new technologies.

Human Rights and Fintech: Key Issues

Discriminatory Products and Services

Fintech is often powered by AI-driven technologies, which can help determine the financial risk of lending to retail customers or small business owners. However, when AI algorithms are trained on historical or unverified data, it can lead to biased, discriminatory, or nonrepresentative outcomes for customers. Unless data integrity is proactively addressed, AI-driven financial models or predictions may become poisoned or corrupted, leading to unfair and harmful outcomes. This includes denying or offering products and services with unfair terms and rates, based on an individual’s race, sex, marital status, or other protected characteristic.

Examples of human rights implicated: Right to be free from discrimination and to enjoy equal rights regardless of nationality, place of residence, sex, gender identity, sexual orientation, national or ethnic origin, color, religion, language, or any other status

Fraudulent or Misleading Marketing and Lending Practices

By expanding access to financial markets, fintechs are engaging new customers who may have lower financial literacy or are more vulnerable to fraudulent, unfair, or deceptive practices. Fintech marketing might promote easy access to capital due to its convenient and quick digital loan application processes, but it can come with hidden fees and exorbitant interest rates that perpetuate cycles of poverty and indebtedness. Without proper internal controls and regulatory oversight, fintech can cultivate an environment where bad actors can fleece and erode fintech’s benefits for customers, including “unbanked” and other people who are historically excluded from the formal financial system.

Examples of human rights implicated: Right to access information and freedom of expression; right to a decent standard of living

Data Breaches

A key element of fintech’s value proposition—the reliance on digital platforms, online applications, and cloud services—can actually increase fintechs’ exposure to cyber threats. Potential vulnerabilities in these tech solutions, combined with the nature and volume of customer data, make fintechs a prime target for cyber-attacks. Hackers can collect highly sensitive financial and other personal information and use this to exploit customers through identity theft, fraud, and other means. Without proper controls and oversight, fintech companies may facilitate the violation of customers’ privacy rights, which may even lead to catastrophic impacts on their financial health and overall well-being.

Examples of human rights implicated: Right to privacy, including protections from malicious and unauthorized use of personal data. Identity theft can also implicate a range of social, economic, cultural, civil, political, environmental, and labor rights.

Corruption, Trafficking, and Other Illicit Activities

Cryptocurrency and other fintech payment platforms with encryption features (typically employed by companies to protect user data) are at risk of being used for illicit transactions, perpetuating human rights risks associated with illegal acts, such as corruption, bribery, and human and other trafficking activities. While corruption and bribery have their own legal and regulatory ramifications, they also have grave social and human rights impacts, often by siphoning off resources from essential public goods and services. In addition, an estimated US$150 billion worldwide is exchanged each year to fund human trafficking activities—often through legitimate financial channels—enabling the exploitation and abuse of vulnerable populations. Mobile payments and cryptocurrency have a high risk of being used for this illicit financial activity because of their often anonymous nature, which makes it harder for law enforcement to detect.

Examples of human rights implicated: Right to be free from slavery, including specific protections related to sex trafficking, debt bondage, and child labor; right to life, liberty and security; right to equal participation in political and public affairs and service; right to a decent standard of living; right to a clean, healthy, and sustainable environment; right to access effective remedy

The rapid and widespread adoption of fintech solutions can compound the risks discussed above, thereby exacerbating and contributing to the further marginalization of individuals traditionally excluded from the financial system. While fintech can expand access to capital and provide innovative financial solutions, it is important that fintech companies address the negative human rights implications associated with their products and services. This is not only beneficial for business and the overall health of the financial system, but also for customers and their communities.

How Fintechs Can Address Actual and Potential Impacts

Based on our work across the financial services and technology sectors, there are some initial steps that fintechs can take to manage these risks and amplify the benefits associated with fintech solutions.

Conduct Human Rights Due Diligence

The UN Guiding Principles on Business and Human Rights (UNGPs) establish the authoritative global framework for business to identify, prevent, mitigate, and account for negative impacts on people and their rights. This framework involves undertaking ongoing human rights due diligence, which can help fintechs more readily identify and address actual and potential impacts associated with the use and deployment of fintech solutions and offer more rights-compatible products and services.

Manage AI-Related Risks and Opportunities through a Responsible AI Approach

Adopt policies, practices, and governance frameworks centered on the ethical and human rights considerations of developing and applying AI technologies. This can include creating internal oversight and review functions related to AI, as well as assessing data inputs, algorithms, and use cases and publicly disclosing use parameters and limitations.

Develop Data Management and Security Measures in Line with “Privacy by Design” Principles

Given the persistence of threats to data security and customer privacy, fintechs should regularly update systems and controls around collecting, storing, using, sharing, or combining customer data using a privacy and data protection by design approach that comports with the highest international standards.

Engage Meaningfully with External Stakeholders

Fintechs can regularly engage with experts, business partners, customers, and communities affected by their products and services to better understand the risks and management gaps and make informed decisions on how to address them based on best practice and emerging regulations.

Enable Access to Remedy

Under the UNGPs and a growing number of regulations, companies are expected to adopt or participate in effective grievance mechanisms that provide a channel for affected stakeholders to report concerns and receive redress for adverse impacts connected to their operations and value chains. These channels provide fintechs with a valuable source of learning that is essential for improved performance, accountability, and social license to operate—the unwritten acceptance and approval by affected stakeholders and the public of a company’s operations and activities.

Contribute to Industry-Level Change

Fintechs can engage in multi-stakeholder platforms and industry dialogues to tackle systemic challenges, such as human trafficking, socioeconomic inequality, and weak regulatory environments that exacerbate financial exclusion and other harmful impacts associated with fintech solutions.

By undertaking these key steps, fintechs can harness the positive potential that fintech solutions offer in a responsible and rights-respecting manner. To learn more about how BSR can help your company manage social and human rights risks associated with its products, services, and business relationships, please reach out to us.

People

Lucie Maria Momdjian

Lucie leads BSR’s creative design work, shaping the organization’s visual identity across all platforms. With expertise in art direction and graphic design, Lucie has extensive experience in developing and executing impactful designs for presentations, reports, marketing materials, websites, direct email campaigns, and events. She ensures brand consistency and brings a…

People

Lucie Maria Momdjian

Preview

Lucie leads BSR’s creative design work, shaping the organization’s visual identity across all platforms.

With expertise in art direction and graphic design, Lucie has extensive experience in developing and executing impactful designs for presentations, reports, marketing materials, websites, direct email campaigns, and events. She ensures brand consistency and brings a storytelling approach to her work, effectively translating BSR’s mission and values into compelling visuals.

Previously, Lucie collaborated with international organizations and NGOs, including Oxfam, World Vision, IRC, WWF, and Fairtrade, among others, to design reports, social media campaigns, and publications. Her portfolio includes projects focused on sustainability, humanitarian aid, and social impact, reflecting her dedication to using design as a tool for positive change.

Lucie holds a BA and MS in Art Direction and Graphic Design from ALBA University in Lebanon, and she is fluent in English, French, Arabic, and Armenian.

Blog | Wednesday March 26, 2025

Democracy and Human Rights: How Businesses Can Uphold the Rule of Law

The Rule of Law is critical for companies because it creates a stable environment where they are more likely to invest, innovate, and thrive. BSR shares ways for business to uphold the Rule of Law.

Blog | Wednesday March 26, 2025

Democracy and Human Rights: How Businesses Can Uphold the Rule of Law

Preview

In a time of geopolitical turmoil and regulatory uncertainty, companies are increasingly seeking clarity and stability to inform their strategies and decision-making at the operational and value chain levels. While market fluctuations and policy shifts are expected over time, businesses rely on a bedrock of fundamental rules and legal norms that govern the economy and society—as well as governments themselves—in a relatively predictable and fair manner. This bedrock, reinforced by democratic checks and balances, establishes a level playing field on which companies can operate efficiently and effectively while upholding their responsibilities to respect human rights and the environment.

The Rule of Law is a set of principles or ideals for ensuring an orderly and just society, and a system under which all people, institutions, and entities (both public and private), including countries and governments, as well as corporate actors, are held accountable. The United Nations further notes that Rule of Law is “fundamental to international peace and security and political stability; to achieve economic and social progress and development; and to protect people’s rights and fundamental freedoms.” It is inextricably linked not only to the protection and the promotion of human rights, but also to upholding the underpinnings of democracy itself.

Key elements of the Rule of Law include accountability, transparency and openness (particularly from governments), just laws, and accessible and impartial justice and justice systems, which form the foundation for the predictability and certainty that enable business to operate with confidence. In the realm of business and human rights, this can look like ensuring accountability when human rights are violated by businesses, providing equal protection from negative human rights impacts of corporate activities, maintaining transparency in decision-making, providing access to judicial protections when rights are violated by businesses, protecting property rights (including intellectual property), enforcing fair contracts, and upholding respect for human rights by States and businesses.

The Rule of Law is critical for business because it creates a stable environment in which companies are more likely to invest, innovate, and thrive. When the Rule of Law is strong, companies can be more certain that the rules will be applied evenly and that all actors will be held accountable for failing to follow them, including for human rights and environmental harm. Instead of a system that unfairly protects and favors the few, the Rule of Law establishes a level playing field by suppressing corruption and fostering competition. It brings certainty to contracts and property rights and catalyzes a legal framework for impartially resolving disputes in a relatively accessible and transparent way. This not only provides fertile ground for economic prosperity but also encourages respect for human rights and social cohesion, which allows individuals and communities to more meaningfully participate in decisions that affect their daily lives and benefit from this prosperity.

The UN Guiding Principles on Business and Human Rights (UNGPs) establish that States protect and businesses respect human rights. Strengthening corporate adherence to the UNGPs is aligned with the promotion of the Rule of Law, as the UNGPs aim to ensure that businesses operate within a broader system that respects human rights, essentially directing companies to uphold the Rule of Law when conducting their operations, particularly in areas where a strong Rule of Law may be lacking. In so doing, the UNGPs affirm that businesses be accountable for their actions, and that neither they, nor the States in which they operate, are above the law.

Specific actions that businesses can take, such as respecting and promoting the rights of Human Rights Defenders or mandating accountability when doing business in conflict-affected and high-risk areas, are inherently linked to the Rule of Law. Furthermore, companies can adopt policies with expectations and requirements for responsible business conduct and adherence to legislation and the Rule of Law. Businesses can also undertake responsible political engagement to advance the Rule of Law and its principles.

The long path of supporting democracy by upholding the Rule of Law can begin by business actors evaluating their practices, actions, and policies, both internal and external, through the prism of the UNGPs. Relatedly, the UNGPs can serve as an interpretive guide for how to responsibly operate during polarized and changed circumstances, in which democracy and human rights are the North Star. At the very core, the human rights-based approach of the UNGPs can inspire and empower businesses to support and uphold the Rule of Law by holding governments, including their own, and business actors, regardless of their size, accountable and reaffirming that no one is above the law.

To learn more about concrete steps your company can take to advance human rights and align with the UNGPs, please contact BSR's Human Rights team.

Reports | Thursday March 20, 2025

Resilient Business within Planetary Boundaries

Achieving global (and corporate) sustainability goals presents an opportunity for business, but attaining these goals requires systematic change. BSR provides practical guidance on impactful transformation that will deliver thriving business over the long term.

Reports | Thursday March 20, 2025

Resilient Business within Planetary Boundaries

Preview

Over the past couple of years, BSR has engaged in conversations with member companies that face an increasing tension between achieving their sustainability goals and meeting business growth imperatives.

Many companies have moved past incremental changes and easy-to-implement measures. Achieving global (and corporate) sustainability goals presents an opportunity for business—but attaining these goals requires systematic change.

These reports are part of BSR’s response. They are designed to provide practical guidance, resources, and examples to accompany business leaders across functions to capture the opportunity to deliver thriving business over the long term.

Insights+ | Monday March 10, 2025

EU Omnibus: It’s Time to Shift Focus from Compliance to Impact

EU Omnibus: It’s Time to Shift Focus from Compliance to Impact

Insights+ | Monday March 10, 2025

EU Omnibus: It’s Time to Shift Focus from Compliance to Impact

Preview

Blog | Wednesday March 5, 2025

Beyond International Women’s Day: Enduring Actions for Global Business in a Turbulent Time

As we approach International Women’s Day, what steps can companies take to promote women’s equality in their everyday business operations?

Blog | Wednesday March 5, 2025

Beyond International Women’s Day: Enduring Actions for Global Business in a Turbulent Time

Preview

To use a trending metaphor these days—the progress of women in every sphere is at a fork in the road. Unleashing the full potential of women and girls could add more than $12 trillion dollars to global GDP, drive productivity and the bottom line, and support families and communities around the world. Simultaneously, rising populism and rollbacks in democracy globally correlate with threats to women's equality in every domain, which is having a chilling effect on what actions the private sector takes internally and externally.

According to the World Economic Forum’s Global Gender Gap Report 2024, it could take five generations or 134 years to achieve full parity worldwide. This is an incalculable amount of lost revenue, productivity, and innovation. There is no shortage of research and business case-making that unpacks the causes of these chronic gaps and implications of diminished opportunity by gender.

Overall, women’s employment worldwide has surged past pre-pandemic levels. However, increased representation of women in leadership at companies has largely stalled. Let alone workplace policies that would unleash greater participation and productivity among women at all levels of work.

Recent high-profile campaigns—such as those seen during the Super Bowl in the U.S. or on statues in the U.K. or in publications across India—have reignited discussions on gender equity, challenging outdated norms and spotlighting barriers to opportunity on a massive scale. These manufactured flashpoints, often supported by businesses in different ways, can help raise awareness but any actual impact comes after the spotlight fades.

With company initiatives and workplace policies facing backlash and budget pressures, business leaders need to wrestle with the reality: the scrutiny that symbolic gestures and commemorative celebration invites make companies less inclined to talk about the challenges. But what enduring actions can companies take that embed opportunity into business operations?

- Assessment as part of intervention. The Women’s Empowerment Principles Gender Gap Analysis Tool is a guide designed to help companies from around the world assess gender equality performance across the workplace, marketplace, and community. This free tool helps companies of all sizes and industry inventory their current efforts and understand benchmarks to inform meaningful goals. The questionnaire itself can be a useful intervention.

- Tap existing competencies where they exist, such as adding a gender lens to existing human rights tools. Roadmaps and case studies are readily available. Furthermore, as companies adopt AI in new and untested ways, practitioners can integrate human rights principles and human rights assessment (HRA) approaches by bringing an explicit gender lens.

- Pay equity as the baseline. Conduct a wage equity audit and make the adjustments needed to achieve fair and equitable pay at all levels and in all countries.

- Commit to paying a living wage. The national minimum wage in the U.S. hasn’t been raised in 15 years, let alone kept up with inflation. Wages vary depending on states and disparity across global regions. Companies are setting standards for their workplaces and across the value chain.

- Offer paid sick time and paid family and medical leave. Workers need access to paid sick time for when they are ill or must-see health care professionals, especially if they have to travel long distances or wait to see providers. Recently, decreased access to reproductive healthcare in the U.S. has driven companies to find ways to increase benefits and programs to enable access to care. Employees also need access to paid family and medical leave for themselves or family members who may need assistance at various stages of life. While state and country requirements vary, employers can set a standard for their workplaces, especially where laws leave gaps.

- Continue to expand supply chains with expansive procurement processes. Companies can continue dedicated efforts to scout and make joining corporate supplier programs easier, especially for emerging vendors. Procurement is an important tool companies can wield to build economic inclusion and can contribute to consumer loyalty.

- Bring the perspectives of women into boardrooms. Consider executive as well as frontline employee representation on the corporate board to prevent blind spots and inform governance decisions. In some global regions, such representation is required, whereas some companies have experimented with employee advisory boards or other ways to tap existing employee voice (ERGs, unions) to gather inputs.

- Support community-level and systemic change. Companies can assess their prior philanthropic and social impact commitments alongside existing unmet needs facing employees and customers in communities where they operate. Companies can help advance reforms when it comes to public policy and even regulations that support fairness and economic inclusion for everyone. For example, companies can support spending on infrastructure like transportation and housing—issues that directly impact the ability of women to work and care for families.

Leading with Purpose Every Day

This International Women’s Day serves as a reminder that supporting women in the workplace shouldn’t be confined to the calendar. Companies can prioritize meaningful action over performative gestures, creating lasting impact year-round. This approach not only fosters a more inclusive environment but also contributes to long-term success and resilience of businesses and nations.

Blog | Wednesday March 5, 2025

Managing Migrant Labor Human Rights Risks in U.S. Food Value Chains

Against a backdrop of labor shortages and persistent challenges with existing legislation, BSR experts share their recommendations for managing human rights risks for migrants across U.S. Food, Beverage, and Agriculture supply chains.

Blog | Wednesday March 5, 2025

Managing Migrant Labor Human Rights Risks in U.S. Food Value Chains

Preview

The global agricultural sector is inextricably linked with migrant labor. According to the United Nations Network on Migration, of 281 million international migrants, 169 million work across agricultural value chains. This is particularly true in the United States, where around 70 percent of farmworkers are immigrants, of which 40 percent are undocumented. While many businesses in the food, beverage, and agriculture (FBA) sector depend heavily on migrant workers, both workers and employers are currently facing great uncertainty as the new U.S. administration implements severe measures to curb migration and enact mass deportations. Amidst fierce debates that span national security, job preservation for Americans, ongoing labor shortages, and persistent challenges with existing legislation like the H-2A program, the state of migrant labor across the American FBA sector is at a precipice.

The United States has typically been classified as a low-risk country for labor rights abuses, but with increasing visibility of labor abuses in the U.S., businesses are struggling to manage such risks. Some of these stem from the failures of the H-2A visa program, a temporary work program established to address labor shortages in American farms. H-2A workers have experienced severe labor rights violations, including wage theft, illegal fees, and unpaid hours.

Despite a 50 percent increase in H-2A visa holders from 2018 to 2023, labor shortages in the FBA sector persist. These shortages have even contributed to cases of child labor, since youth, most of whom are migrants, may end up filling cheap labor jobs that power American food production. Migrants take on these jobs because there has been a steady decline of Americans working in agriculture, and the intensive work and exposure to the elements are not the only reasons behind this decrease. Farm workers have notoriously been unprotected by fundamental rights, including overtime pay, minimum wage protections, workplace safety protections, and the right to unionize, which are guaranteed to other workers in the U.S. Even when labor standards exist, agencies enforcing them are underfunded, meaning that worker safety, poor living conditions, or missing pay are rarely addressed. Due to farm labor shortage, U.S. growers have lost US$3.1 billion in additional fresh produce sales per year.

A dramatic increase in migrant deportations may worsen two interconnected characteristics of the agricultural sector: labor shortages and poor working conditions. Enforcement-only approaches to immigration, such as border security and deportation, will severely reduce labor availability in the agriculture sector and could lead to a 1.5-9.1 percent increase in prices overall for consumers. Due to their fragile legal status, the threat of deportation also makes migrants more vulnerable to exploitation in the form of wage and safety violation, sexual harassment, violence, and more. The impact of these deportations is likely to ripple further throughout the economy, with an anticipated rise of 3 percentage points in inflation and a 7.4 percent reduction in GDP by 2028.

Despite some efforts to address migrant labor risks like protecting H-2A visa holders from employer retaliation, there have been significant pushbacks, including recent roll backs of child labor and other labor protections in agriculture. The failure to evolve legislation to ensure rights for workers unfortunately puts the onus of managing a vulnerable labor force, with inherent child and forced labor risks, onto farmers and FBA companies rather than government regulators.

For companies navigating this turbulent time, investing in human rights due diligence and staying in alignment with the United Nations Guiding Principles for Business and Human Rights and the OECD Guidelines for Responsible Business Conduct are key to meeting these evolving challenges. Even as administrations change and regulations shift, these frameworks provide a consistent long-term approach to navigating human rights risks that could otherwise have legal, reputational, and even financial implications.

For more immediate action, here are several recommendations for managing human rights risks for migrants in your U.S. FBA supply chains:

- Rapidly assess the labor risks in your sourcing and production regions based on areas with a high prevalence of migrant labor. It is also worthwhile to identify states and/or regions where labor law and enforcement for agricultural workers are weak, potentially another indicator of greater risk. Monitor high-risk areas and employ locally relevant interventions as needed. Useful tools to help prioritize your efforts are Farmworker Justice’s evaluation of worker compensation by states, the Pew Research Center’s research on undocumented immigrants in the U.S., and Oxfam’s Best States to Work.

- Evaluate your management systems for human rights risks with U.S. operations and suppliers. This includes reviewing your Supplier Code of Conduct and audit efforts. Consider the discrepancies that may exist between your company policies and local state laws. If you haven’t already, conduct a human rights assessment to identify your salient human risks. Create more opportunities for dialogue with suppliers to discuss labor challenges and conduct more site visits to farms and facilities. When risks are identified, work with local stakeholders or a labor rights partner to determine the best course for remedy.

- Recognize and address the limitations of current audit practices through targeted initiatives. Consider engaging with programs like the Coalition of Immokalee Workers’ Fair Food Program, which employs a worker-driven social responsibility model to ensure humane wages and working conditions for farmworkers. The Equitable Food Initiative offers a rigorous social responsibility certification, implementation programs, and public tools, and its labor standards were developed by a multistakeholder group of unions, consumer groups, employers and retailers in 2013. It is aligned with the Ethical Charter on Responsible Labor Practices, an initiative to collaboratively strengthen labor practices in U.S. fresh produce value chains that are already supported by a number of leading American retailers and producers.

- Pay particular attention to issues of forced labor, child labor, freedom of association, and living conditions for workers in agricultural supply chains. Inform your procurement team of these issues and make sure it is a topic that they are raising with suppliers. Learn how to engage with suppliers to address risks. For instance, UNICEF USA’s recent report on child labor in the U.S. provides guidance for companies on addressing child labor violations in U.S. supply chains, including a compliance framework and recommendations that can help companies stay aligned with both international standards and U.S. regulations.

- Engage with industry and multi-stakeholder initiatives. AIM Progress has a working group on child and forced labor in U.S. food manufacturing that recently produced an e-learning course with Verité that is being used to build capacity with American suppliers. The Consumer Goods Forum’s Human Rights Coalition works on responsible recruitment and employment, human rights due diligence, and collaboration between companies. Two BSR Collaborative Initiatives, the Human Rights Working Group and the Global Business Coalition Against Human Trafficking, also support companies in navigating emerging human rights risks.

BSR is already partnering with its members on specific approaches to address human rights risks in the FBA sector, and it continues to support efforts for broader exchange and engagement. To discuss these issues and discover opportunities to engage, email [email protected].

Blog | Wednesday February 26, 2025

Protecting Children in the Digital Environment: The Role of Impact Assessments

BSR Technology and Human Rights experts discuss the benefits of conducting a Child Rights Impact Assessment and key takeaways from their recent report.

Blog | Wednesday February 26, 2025

Protecting Children in the Digital Environment: The Role of Impact Assessments

Preview

There is more awareness of the impact of technology on children than ever before. Despite the many benefits that digital technology provides to children (e.g., access to education, free expression, and maintaining social connections), concerns are rising around the adverse impacts on mental health, attention, and protection from harm.

In 2023, Amazon entered a US$25 million settlement with the US Department of Justice and Federal Trade Commission over charges related to children’s privacy. In 2024, concerns about children and social media platforms regularly made headlines. State attorneys general in the US sued social media companies alleging harms to children’s safety and well-being. The US surgeon general called for warning labels on social media platforms, and several tech CEOs publicly apologized to parents whose children were harmed by social media.

In response, regulators have begun to take action to address these harms. The UK passed an Online Safety Act that requires online platforms to prevent children from accessing age-inappropriate or harmful content. In Australia, efforts to protect children from harm has resulted in a social media ban for children under 16. Companies developing and deploying tech tools are being required to take stock of their impacts on children’s rights and the effectiveness of their measures to address such impacts.

While companies, governments, and civil society actors are increasingly invested in addressing the adverse impacts of technology on children, approaches remain inconsistent and fragmented. Research shows that company approaches are often focused on protection issues (e.g., illegal content and freedom from exploitation or sexual abuse) and responding to legal mandates, which may cause issues related to children’s participation in the digital environment (e.g., freedom of expression or access to culture) to be overlooked. Furthermore, current approaches to assessing impacts on children are often seen by companies as a "one-and-done" exercise, rather than an ongoing process that integrates external perspectives and evolves as new technologies and use habits arise.

Several factors complicate our ability to fully understand and mitigate the adverse impacts of technology on children, including the rapid pace of technological advancement, regulatory discrepancies across different jurisdictions, and the limited availability of data about children across diverse ages, socioeconomic statuses, gender identities, geographies, and individual circumstances. As a result of these challenges and the gaps in their current approaches, companies fail to track and mitigate evolving risks to children.

Child Rights Impact Assessments

Companies have a responsibility to identify and address adverse human rights impacts associated with their operations, products, and services.

To assess impacts to children in particular, companies can conduct Child Rights Impact Assessments. CRIAs are an effective way for companies to systematically evaluate their impacts on child rights as defined in the Convention on the Rights of the Child, and other internationally accepted human rights and child rights instruments. Similar to a Human Rights Impact Assessment, the CRIA uses a methodology informed by the UN Guiding Principles on Business and Human Rights (UNGPs) and seeks input from rightsholders to identify a company’s impacts on children’s rights, prioritize these impacts based on their severity, and determine appropriate action to address them.

In 2023, UNICEF engaged BSR to explore how companies are leveraging CRIAs and help develop a CRIA tool that companies operating in the digital environment can use to systematically identify, assess, and address their impacts on child rights. The project involved extensive research into existing resources to assess companies’ impacts on children, a review of current CRIA tools and practices, an assessment of child rights considerations in new regulations, and engagement with 130 stakeholders.

BSR has published a paper that brings together key findings from this research, as well as our observations on how companies are currently approaching child rights impact assessments in relation to the digital environment. It is a precursor to the digital environment CRIA tool that UNICEF will publish in 2025.

Benefits of Conducting CRIAs

BSR’s review of the current landscape showed that while many companies seek to understand their actual and potential impacts on children in the digital environment, few use CRIAs to do so. For companies operating in the digital environment, CRIAs can be a helpful tool for several reasons:

- CRIAs allow companies to assess their impacts against the full list of child rights. Assessing against a comprehensive list of rights ensures that key issues or new impacts are not overlooked and constitutes a defensible methodology that is grounded in international human rights instruments.

- CRIAs can enable age-appropriate design through early consideration of risks and opportunities. Proactively engaging stakeholders and identifying the potential risks/opportunities allows companies to integrate these considerations into the design of a technology product and address harms before they become more severe, which can happen quickly in the digital environment.

- CRIAs can support companies’ regulatory compliance efforts. Regulations like the EU Digital Services Act, UK Online Safety Act, Australian Online Safety Act, and the Corporate Sustainability Reporting Directive require companies to assess risks to people, including children, and implement mitigation measures. CRIAs can help companies address these requirements by aligning with UNGPs due diligence approach and integrating findings into broader human rights and regulatory risk assessments.

As the digital environment continues to shape children’s lives and regulatory expectations continue to grow, respecting, protecting, and fulfilling child rights should be a priority for all businesses that engage with digital technologies—whether they are developers, deployers, or users. UNICEF’s development of a CRIA tool specific to the digital environment is a critical step in that process.

Explore BSR’s full report for detailed insights on why CRIAs are an essential practice and what to expect from UNICEF’s forthcoming tool.

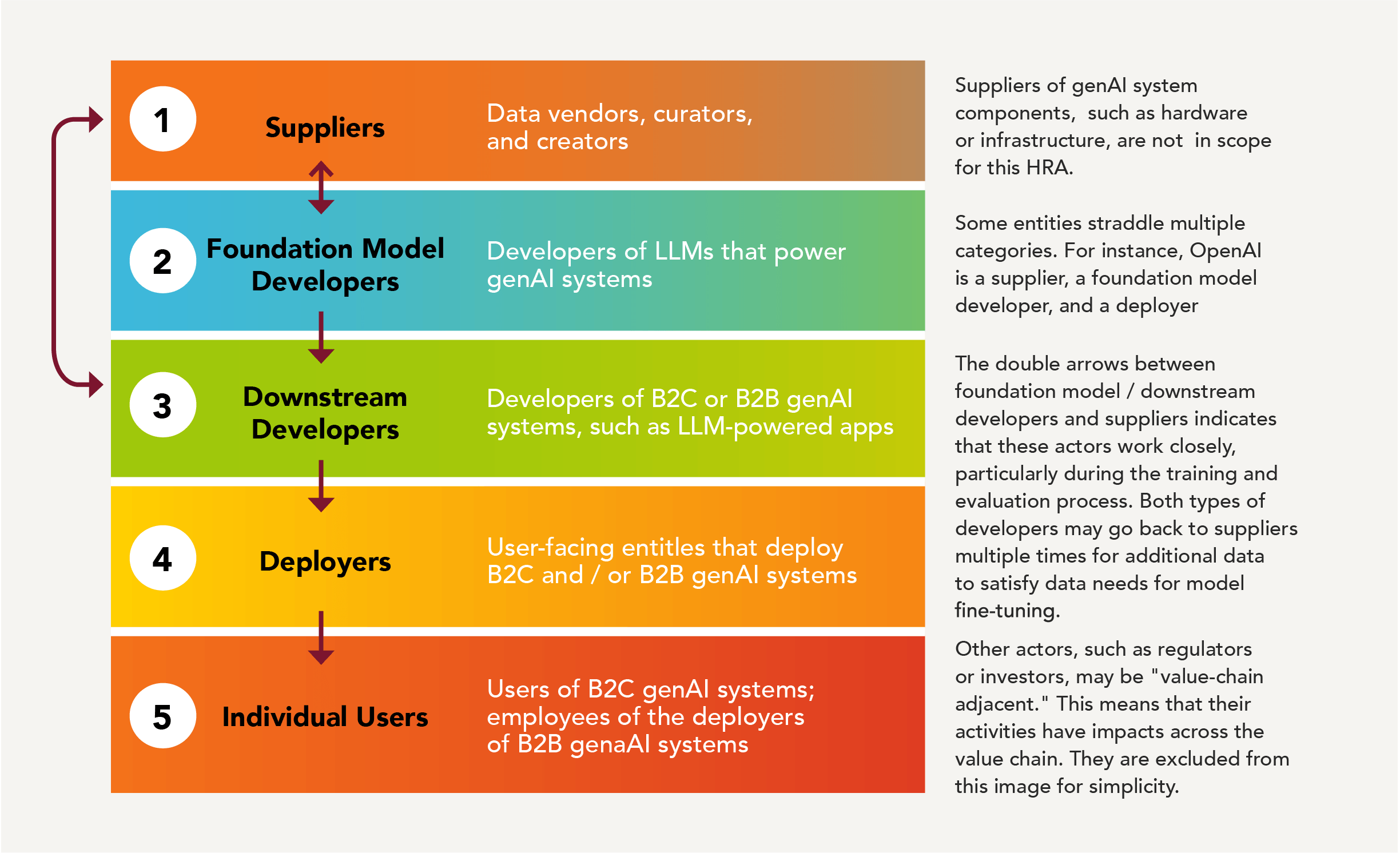

Reports | Tuesday February 25, 2025

Human Rights Across the Generative AI Value Chain

This Human Rights Assessment shares how decisions made across the generative AI value chain can impact human rights. The report also includes practitioner guides on incorporating a human rights-based approach for people working on responsible AI.

Reports | Tuesday February 25, 2025

Human Rights Across the Generative AI Value Chain

Preview

As the capabilities of generative AI (genAI) increase daily, they also pose risks to people and society. While some companies have created AI governance systems to address these risks, many of these systems do not adequately integrate human rights principles and methodologies, or do not include them at all. Additionally, genAI's "value chain" involves an interconnected web of suppliers, vendors, individual users, foundation model developers, etc., where decisions made by one actor may have consequences on the others. As a result, to properly assess the human rights impacts of genAI, its entire value chain must be considered.

To assist responsible AI practitioners and encourage greater transparency in the field of human rights and genAI, BSR conducted a human rights assessment that identifies and assesses the actual and potential human rights impacts (i.e., risks and opportunities) associated with genAI through a value chain lens. It shows how different value chain actors, listed in the diagram below, are connected to potential impacts and recommends actions they can take to address risks and provide remedy for harms.

Click on the image to view a larger size

Accompanying this assessment is a series of practitioner guides that advise those working on responsible AI on how to incorporate a human rights-based approach to their work. These guides can be used across all AI product development and deployment.

- Overview of Responsible AI Practitioner Guides

- Guide 1: Fundamentals of a Human Rights-Based Approach to Generative AI

- Guide 2: Governance and Management

- Guide 3: Impact Assessment

- Guide 4: Risk Mitigation

- Guide 5: Conducting Stakeholder Engagement

- Guide 6: Policies and Enforcement

- Guide 7: Aligning Transparency and Disclosure Practices with Human Rights Responsibilities

- Guide 8: Remedy for Generative AI-Related Harms

Search Again?